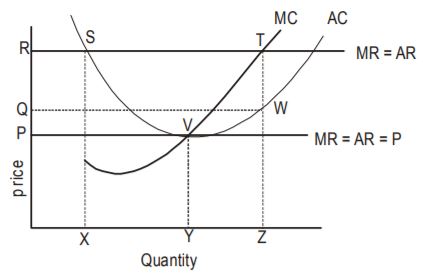

The long-run equilibrium price and quantity forthe firm are respectively

Options:A) OP, OY

B) OR, OZ

C) OR, OX

D) OQ, OZ

Show Answer

The correct answer is C .

A) P = 12, Q = 16

B) P = 15, Q = 10

C) P = 12, Q = 14

D) P = 16, Q = 12

Show Answer

The correct answer is D .

A) public service

B) worker's union

C) rate of inflation

D) supply and demand for labour

Show Answer

The correct answer is D .

A) more naira is spent on commodities with the highest utility

B) less naira is spent on commodities with the lowest utility

C) the utility of the last naira spent on each commodity is equal

D) the amount spent on each commodity is equal

Show Answer

The correct answer is C .

A) Wages earned by doctor

B) Rent paid to landlords

C) Indirect tax

D) Undistributed company profits

E) Interest on loan

Show Answer

The correct answer is C .

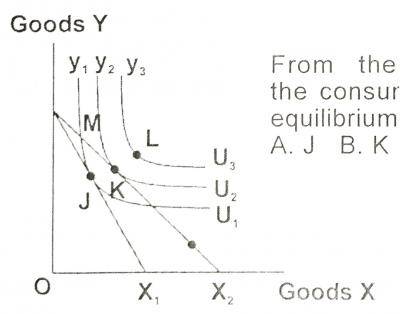

From the graph above the consumer will attain equilibrium at point_______________

Options:A) J

B) K

C) M

D) L

Show Answer

The correct answer is B .

A) exploration of crude oil

B) refining of crude oil

C) marketing of finished products

D) management of pollution

Show Answer

The correct answer is A .

A) what is and not what should be

B) facts and not figures

C) facts and figures

D) value judgements

Show Answer

The correct answer is D .

A) retailing

B) dumping

C) internal trade

D) advertising

Show Answer

The correct answer is B .

A) the demand for money is inversely related to the rate of interest

B) investment is directly related to the rate of interest

C) investment is not related to the rate of interest to the rate of interest

D) the demand for money is directly related to the rate of interest

Show Answer

The correct answer is D .